With ringing in the new year comes the inevitable resolutions to be happier, healthier, more productive…all good intentions. But, what if this year you make a different kind of resolution—an actionable goal that could make a difference in the causes you care about? How about a goal that goes beyond yourself and could also have a positive impact on your community? This year I implore you to make at least one charitable giving goal. A giving goal can be a “resolution” you actually keep after the snow melts. How? With the right plan in place!

Similarly, I encourage my clients to determine their estate planning goals. These goals help guide me in drafting a personalized estate plan and determining which documents and provisions are needed. After all, every Iowan, family, and business is unique. Charitable giving goals can work the same way as a guiding blueprint for the who, what, when, and why of giving.

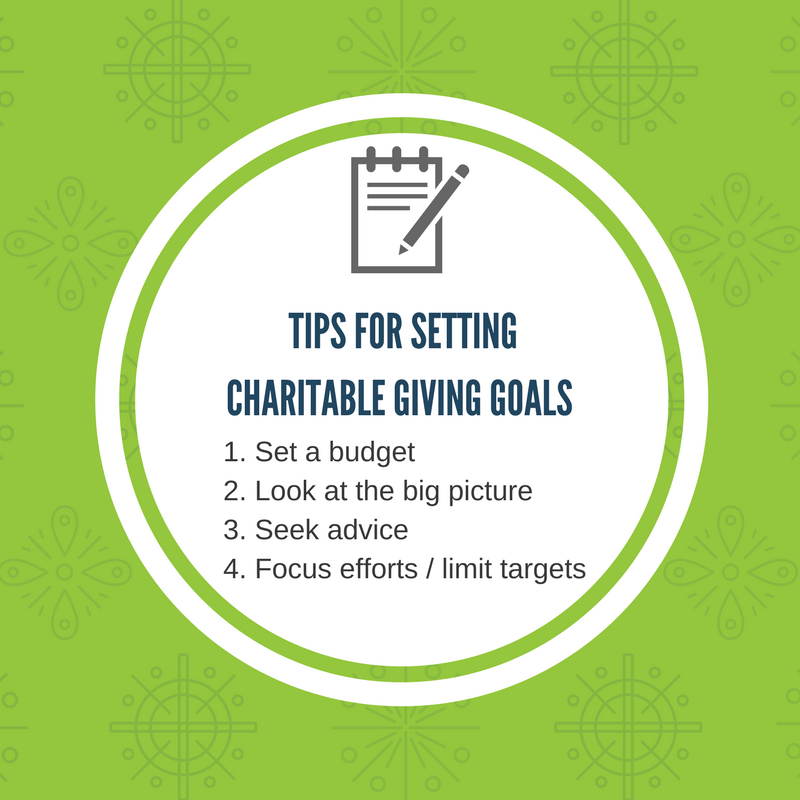

Use the following information to set your charitable giving goals for the new year!

Set a budget.

Of course, to begin, you’ll need to examine your entire budget including income, committed expenses (such as rent/mortgage payments, all bills, healthcare costs, etc.), to determine your discretionary income—this is the money you have left over after your committed expenses.

Along with your budget you should also consider whether larger one-time donations or recurring (perhaps monthly) donations work better for your budget, personality, and spending habits. A one-time donation may help prevent money from being spent on other discretionary choices. On the other hand, a repeated, monthly donation may help divide the total amount up into manageable sums. And, monthly donations can often be configured to automatically be made from your account which makes it easy to set the figure at the beginning of the year and make it a regular expenditure. Nonprofit organizations are grateful for all charitable contributions, but recurring, monthly gifts make their budgeting easier.

Look at the big picture.

Step back from the accounting weeds for a moment and sit down with a plain piece of paper. Write down the causes and organizations you care about. If you feel passionate about a certain issue, but don’t know of a specific charity off the top of your head that is addressing the issue, make a note of it. Your list doesn’t have to be long, just true to you.

Then, commit to research to determine which organizations are going to invest your money toward a mission that aligns with your own ethos. Some things to consider about a charity:

- Financial health. Tax-exempt organizations have to file Form 990 (officially, the “Return of Organization Exempt From Income Tax”) with the IRS. This form details the organization’s financial information and is available to the public. Do a search on a database such as the Foundation Center, for a charity you’re considering donating to, and review the financial data.

- What’s the charity’s commitment to transparency? How about accountability?

- What’s the organization’s Charity Navigator rating, if any? Charity Navigator’s rating system examines a charity’s performance in the areas of financial health and accountability/transparency, and presents it in an easily discernible way.

- Is the organization a public charity or private foundation? This will have an impact on your federal income tax charitable deductions.

- Is the organization based in the U.S. or is it a foreign charity? (Generally, if the donee is a foreign charitable organization, an income tax deduction is unavailable.)

Of course, if you’re personally involved with an organization through volunteering, fundraising, or the like, that’s a good way to “know” the charities as well. Research will empower and embolden your charitable goals if you know your donation is going to an upstanding, trustworthy operation.

Seek advice.

If you made a goal to increase muscle mass, you would likely seek the services of a personal trainer. If your goal is to eat healthier? Maybe a nutritionist. When the goal is to be committed to smart charitable donations, you’ll want to enlist the likes of your lawyer, accountant, and/or financial advisor. Seek out a professional who has experience working with nonprofits, the tax code, and strategies for intelligent giving. This pro can and should be able to help you put your plan into action.

(This tip also applies to practicing charitable giving through your estate plan—something you should definitely hire an estate planning lawyer to make sure the estate plan is properly, legally executed.)

Focus efforts / limit charitable targets.

Smart charitable giving means a vested commitment toward a cause or organization’s advancement, as well as financially beneficial tax deductions for you. Unlike investments where the general advice is to diversify to reduce risk, in the realm of charitable giving the opposite may well be true. You may well receive the greatest “return” by concentrating your giving on a fewer, rather than more, organizations. Consider giving to two or three nonprofits to magnify your impact.

If you’re ready to commit to charitable giving goals you can actually keep I’m happy to offer advice and strategy. Don’t hesitate to reach out via email (gordon@gordonfischerlawfirm.com) or by phone (515-371-6077).

Giving is a privilege

Giving is a privilege