There is a rumor that has been floating around that only the rich need estate planning. That is extremely false. Everyone needs an estate plan, but the wealthy don’t need estate planning as much as the middle-class and working-class folks. If this contradicts everything you’ve ever thought about estate planning allow me to explain.

The Case of Kingston Lear

Suppose Kingston Lear (get it?!), a wealthy Iowan, decides he doesn’t need a qualified and experienced estate planner, he can do it himself, or use an online, one-size-fits-all service. Hey, Lear figures, this way he’s saving both time and money. Also, nothing is going to happen to him for a while, he can get around to doing a proper estate plan with a proper estate planning professional “someday.”

Of course, “someday” never comes, but Lear’s death does. His three daughters are aghast that Lear has no real estate plan. The template resembling an estate plan is completely inadequate for the size and complexity of Lear’s assets.

A Matter of Trusts

Lear could have easily, with the help of a professional advisor, set up a trust (even a plain, “vanilla” revocable living trust would have worked) to avoid probate. But, the online service he used didn’t even explain the difference between wills and trusts. So, Lear’s assets all must go through probate. This means that the time and money Lear though he was saving is gone in a flash.

Probate Costs and Fees, If You Please

Probate fees are going to equate to at least 2% cut of Lear’s estate. Remember, Lear’s estate is large and complex and valued at $10 million, so the actual figure is probably going to be more like four percent.

Using 4% as the figure for probate fees means a loss of $40,000 ($10 million X .04 = $400,000). This is $400,000 that could have been passed down to his daughters through a trust, or split generously between his heirs and charitable organizations near and dear to Lear’s heart.

Also, court costs may amount to another 1%, or loss of $10,000 more ($10 million X .01 = $100,000).

Loss of Privacy

Another major benefit of a trust—again, not explained to Lear because didn’t seek any individualized advice—is privacy. A will (or most any document that goes through probate, absent very special circumstances) is simply a public document. Anyone can read, copy, share, and write about it.

Consider one of Lear’s major assets was an ongoing business—a Shakespearean-themed jousting complex, where families could have fun practicing jousting.

Unfortunately, in some of the probate papers, it was disclosed that there had been numerous complaints by the Iowa Horse Association about the treatment of horses. It isn’t long until this hits the blogs, and some of the more sensational aspects of the report (though hotly disputed) goes viral. The jousting park, which had been quite profitable, is now eschewed by all the good people of the area. The daughters are forced to sell the business asset to preserve the family’s good name (or what’s left of it) and sell at a loss. While the jousting park had been worth as much as $1 million, the daughters have to sell, so there’s a “paper loss,” but nonetheless less a loss, of another $900,000.

Loss of Future Profits

The $900,000 is a conservative figure; it doesn’t include lost future profits. If not for the scandal becoming public, who knows how long the jousting park could have remained really popular and this profitable. Years? Decades? It’s quite difficult to quantify, but it’s certainly probable that there are some lost profits. The question is: how much?

Costs of Cases

Because Lear’s will wasn’t drafted by professional, there are many ambiguities and loopholes. It’s not long before the three daughters begin fighting and, with unclear direction from their father, they wind up suing each other.

Taking a court case all the way to trial can easily mean $50,000 in attorney’s fees, plus each daughter will want and need her own attorney. So, another $150,000 is lost to attorney’s fees!

Total Losses Equal?

Lear could have had his estate plan done by an Iowa professional for a few thousand dollars. Instead, he lost a total far greater than that:

- Probate Fees: $400,000

- Probate Court Costs: $100,000

- Loss on Sale of Jousting Park: $900,000

- Loss of Future Profits of Jousting Park: Incalculable?

- Attorney’s Fees for Daughters’ Litigation $150,000

This is a hit for the inheritance of $1.55 million, leaving $8.5 million (rounded up), or a little less than $3 million per daughter. But you know what? That still leaves an inheritance of $8.5 million to be split amongst three sisters.

The Rich Can Afford Bad Estate Planning

Lear acted unwisely, arguably recklessly! A great deal of his money was wasted that could have been used for great charitable work in Iowa through local nonprofit organizations. But, for all his foolishness, Lear’s daughters still end up with $3 million each. Will the daughters incur much suffering with “only” $3 million? No.

That’s the rub; the rich can afford to make big (and small) estate planning mistakes.

You Can’t Afford Poor Quality Estate Planning

Let’s look at this from a normal Iowan perspective. At least 2% in probate costs and fees, a huge drop in value in a key asset, attorney’s fees for litigation…can a middle-class estate merely shrug these kinds of losses off? Not a chance.

The rich aren’t like you and me. They can badly botch estate planning. You and I can’t afford to make mistakes with our estates; there’s no room (and not enough money!) for error.

Need an estate plan but aren’t sure where to start? It’s easy from start to finish. Fill out my obligation-free Estate Plan Questionnaire or contact me.

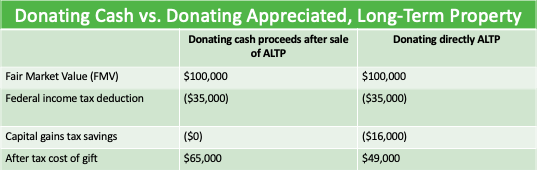

Federal Income Tax Charitable Deduction

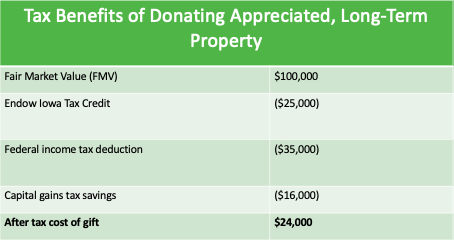

Federal Income Tax Charitable Deduction